It’s Time to Look More Carefully at “Monetary Policy 3 (MP3)” and “Modern Monetary Theory (MMT)”

This article is for folks who are interested in economics, especially about how monetary and fiscal policy will work differently in the future. It will focus on Monetary Policy 3 (the new type that we will see more of around the world) and Modern Monetary Theory (a recently proposed new approach that has received a fair amount of attention). It comes in two parts. The first part is important for folks who care about such stuff but it’s a bit wonky and the second which shows historical cases is very wonky so feel free to wade into this in whatever depth suits your interest.

Part 1: Understanding MP3 and MMT

When I look at economies and markets I look at them in a mechanical way much like an engineer would look at cause-effect relationships of a machine. To me the economic machine has a limited number of basic cause-effect relationships (see “How the Economic Machine Works”) that can be put together in numerous ways that can lead to an infinite number of combinations, just like the 26 letters of the alphabet can be combined to make up an infinite number of words. More specifically there are two basic building blocks of economic policy, which are monetary and fiscal policy, and under these there are a few ways (taxing and spending for fiscal policy, and interest rates and quantitative easing and tightening for monetary policy) and under each of these there are various ways they can be configured. At the big picture level, monetary policy determines the total amount of money and credit (i.e., spending power) in the system, and fiscal policy determines the government’s influence on where it’s taken from (i.e., taxes) and where it goes (i.e., spending).

To me the most important engineering puzzle policy makers around the world have to solve for the years ahead is how to get the economic machine to produce economic well-being for most people when monetary policy does not work. I don’t mean that monetary policy won’t work at all; I mean that it won’t work hardly at all in stimulating economic prosperity in the ways that we are used to having it stimulate economic activity, which are through interest rate cuts (what I call Monetary Policy 1) and through quantitative easing (what I call Monetary Policy 2). That is because it won’t be effective in producing money and credit growth (i.e., spending power) and it won’t be effective in getting it in the hands of most people to increase their productivity and prosperity. Hence I believe we will have to go to Monetary Policy 3, which is fiscal and monetary policy coordination that is of a form that we haven’t seen before in our lifetimes but has existed in various forms in others’ lifetimes or faraway places. It is inevitable that this shift will happen because it is inevitable that central bankers will want to ease when interest rates are pinned at 0% and when quantitative easing will be ineffective in achieving the goal. I recently refreshed my prior exploration of past cases and future possibilities of such coordination, which I will share below.

Modern Monetary Theory is one of those infinite number of configurations that is in my opinion inevitable and shouldn’t be looked at in a precise way. For those of you who don’t know what Modern Monetary Theory is, it’s described here (link). It’s described differently by different folks so it has slightly different configurations. For example, some might change fiscal policy so that there is a wealth tax that is used to eliminate student loans, and others might change taxes and spending in other ways, and there are an infinite number of ways these changes can be configured that we shouldn’t delve into at this stage because that will drive us into the weeds and the particulars that will stand in the way of seeing the big important things. Also, people who are focusing on MMT as a package will limit their thinking to the specifics of that package rather than thinking about the wider range of MP3 policies to find the best one.

MMT’s most important configuration is the fixing of interest rates at 0% and there is the strict controlling of inflation via the changing of fiscal policy surpluses and deficits, which will produce debt that central banks will monetize. In other words, whereas during the times we have become used to, interest rates moved around flexibly and fiscal deficits (often) and surpluses (rarely) were very sticky so interest rates were more important in producing buying power and the cycles, in the future interest rates will be very sticky at 0% and fiscal policies will be much more fluid and important and the debts produced by the deficits will be monetized. In case you didn’t notice, that is by and large what has been happening and will increasingly need to happen. In other words, interest rates are now pinned near 0% in two of the three major reserve currencies (the euro and the yen) and there is a good chance that they will be pinned there in the third and most important reserve currency (the dollar) in the next economic downturn. As a result, fiscal policy deficits that are monetized is the contemporary stimulation configuration of choice. That existed long before there was a concept called “Modern Monetary Theory,” though MMT embraces it. Putting labels aside, it is certainly the case that the configuration of having 1) an interest rate fixed at around 0%, 2) more flexible fiscal policies with debt monetization to fund the resulting deficits with 3) rigorous inflation targeting exists and is increasingly likely, necessary, and possible in reserve currency countries. An added benefit of this approach is that the money and credit created can be better targeted to fund the desired uses than the process of having the central bank buy financial assets from those who have financial assets and use the money they get from the central bank to buy the financial assets they want to buy. There are many historical cases of this happening (see the 1930s-1940s prewar and war periods which, as you know, I think are analogous), which offer worthwhile lessons about how this was and could be engineered.

The big risk of this approach arises from the risks of putting the power to create and allocate money, credit, and spending in the hands of politically elected policy makers. In my opinion, for these MP3 policies to work well, the system would have to be engineered in a way that decision making would be in the hands of wise, not politically motivated, and highly skilled people. It’s difficult to imagine how the system will be built to achieve that. At the same time it is inevitable that we are headed in this direction.

Looking at Our Thinking about MP3 and MMT

In the following section, I will outline some of my thoughts on what MP3 is likely to look like in more detail, but the main points me and my Bridgewater colleagues believe to be true are:

- We agree with the notion that fiscal policy has to be connected with monetary policy to provide enough stimulus in the next economic downturn. That is because Monetary Policy 1 (based on moving interest rates) is in most cases either unable to happen alone or unable to happen much, and Monetary Policy 2 (based on central banks “printing money” and buying financial assets) has limited power to stimulate. For reasons explained in “Principles for Navigating Big Debt Crises,” as long as countries have their debts denominated in their own currencies, the combination of monetary and fiscal policies would likely work to smooth out economic downturns, and the only things that stand in the way are the limited capabilities of economic policy makers and/or the limited political abilities to do the right things.

- We’ve described the coordination of fiscal and monetary policy as a type of Monetary Policy 3 (MP3)—and this is a critical policy tool when interest rate cuts (MP1) and QE (MP2) have limited effectiveness.

- We think that interest rate cuts and QE will be significantly less effective in the next downturn for reasons we’ve described in depth elsewhere. We also don’t believe that monetary policy is producing adequate trickle-down. QE and interest rate cuts help the top earners more than the bottom (because they help drive up asset prices, helping those who already own a lot of assets). And those levers don’t target the money to the things that would be good investments like education, infrastructure, and R&D.

- Obviously, normal fiscal policy is usually the way we handle those sorts of investments. But the problem with relying on fiscal policies in a downturn (besides them being highly politically charged) is that it is slow to respond: it has long lead times, you have to make programs, concerns over deficits can make it more challenging politically to pass fiscal stimulus, etc.

- Imagine instead if you had taxes operating in a swing way, the same way that interest rates move, so that it could be a semi-automatic stabilizer. If you had a recession you would have the equivalent automatic reduction in taxes. On the opposite end, a tightening would result in a rise in taxes.

- We could imagine semi-automatic increases in investments with high ROI to underfunded areas (e.g., education, infrastructure, R&D) rather than just going through financial markets to the areas that companies and investors find most profitable for them.

- Funding such things with money printed by the central bank means that the government doesn’t have to worry about the classic problem of the larger deficits leading to more debt sales leading to higher interest rates because the central bank will fund the deficits with monetization (QE). As we’ve described several times before and have seen since the 2008 financial crisis, such monetization won’t cause too much inflation. That is because inflation is determined by the total amount of spending divided by the quantity of goods and services sold. If the printed money simply offsets some of the decline in credit and spending that happens in an economic downturn, then it won’t produce inflation, e.g., over the last decade central banks struggled with inflation being too low, not runaway inflation, while they have massively monetized debt.

- The big question is who can be relied on to pull these levers well (central bank? federal government?). These tools have the power to do real good but they also can do real harm if not used responsibly. So the governance and decision rights would need to be carefully engineered. That’s a big topic I won’t get into here.

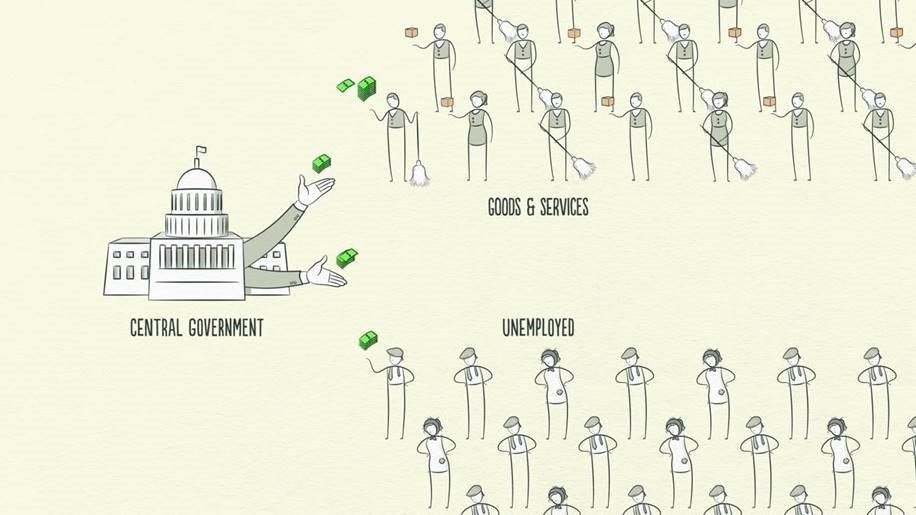

- One specific policy that many MMT proponents have advocated for is a guaranteed jobs program. A lot depends on how that would actually be done. At a superficial level, I like the idea of people working to earn money through a government job in an economic downturn versus just getting welfare checks because staying employed is generally important for people’s psychology/emotional health as well as producing good outcomes (like keeping our cities clean and helping each other).

- There are aspects of MMT that I disagree with. Here are just a couple:

- I disagree with the notion that businesses don’t make investments based on the cost of money and just make decisions based on business prospects. Both the cost of funds and business prospects are important. The cost of capital is a giant influence on the decisions of businesses to do things. For example, the low cost of capital was the reason US companies did huge amounts of share buybacks.

- Some MMTers blame inflation primarily on businesses’ excessive pricing power. While that might influence inflation, the bigger deal is that when you have a shortage of something (labor, commodities, etc.) and excessive demand for it, the price of that thing goes up.

What Monetary Policy 3 (MP3) Could Look Like

As I’ve noted, the policy tools that were sufficient to stimulate the economy in the last several cycles probably won’t be enough this time around. Monetary Policy 1—cutting interest rates—is limited by very low/negative rates across the developed world that probably can’t be lowered all that much more. Monetary Policy 2—quantitative easing—is limited by already very low longer-term interest rates/expected returns on assets and some central banks (especially the ECB) running low on bonds they can buy given current political constraints. Also, it is relatively ineffective in getting money and credit to those who don’t have financial assets, and it contributes to the widening opportunity gap. For these reasons, I believe in the next downturn developed countries will need to turn to “Monetary Policy 3” (MP3). In this study we will 1) define MP3, 2) give examples of it, and 3) focus on what was done in the 1930s.

Monetary Policy 3 comprises monetary policies that are more directed at spenders than at investors/savers (the groups that MP1 and MP2 principally target). In other words, they are policies that provide printed money to spenders with incentives for them to spend it. These sorts of policies will undoubtedly be politically controversial for both central banks and governments. The big question is whether these policies will hurt or help productivity. For reasons explained in the book Principles for Navigating Big Debt Crises, as long as countries have their debts denominated in their own currencies, these policies would likely work to smooth out economic downturns, and the only things that stand in the way are the limited capabilities of economic policy makers and/or the limited political abilities to do the right things, if the productivity produced is more than the amount of money and credit that is produced and spent. That’s why it’s important for policy makers to work through these political/other impediments and develop their “Plan B” now—what they’ll do when MP1 and MP2 don’t provide enough stimulus (e.g., buy equities, buy lesser quality debt, fund fiscal programs, etc.). Otherwise, working through those political considerations as the economy turns down might provide inadequate lead time, which can make the downturn much worse because there is nothing to offset the self-reinforcing downward pressures.

Below, I’ll share some of our prior research on what sort of forms these MP3 policies can take, updated with some recent examples.

Definition of Monetary Policy 3

Though most of us haven’t seen it in our lifetimes, it has existed in other lifetimes and other places. MP3 is a continuum of coordinated monetary and fiscal policies that vary who gets the money (private sector versus public sector) and how directly that printed money is provided (directly providing “helicopter money” to spenders versus more indirect means of financing spending). The following diagram maps many of the possible types of MP3 onto that continuum. In general, the more direct policies would be more effective, but also more politically difficult to do. And some of the least direct policies (or variants of them) have recently been used, but not at the scale that would likely be needed in the next significant downturn.

What MP3 Looks Like

We’ll walk through those policies in more detail (including some historical cases in which the policies were used), starting with MP3 policies that are targeted to the public sector:

- The least direct option is an increase in debt-financed fiscal spending, paired with QE that buys most of the new issuance (e.g., Japan in the 1930s, the US during WWII, and nearly every large developed country following the 2008 financial crisis).

- Central banks could lend to/capitalize development banks or other private/semi-private entities that would use the financing for stimulus-related projects (e.g., China in 2008).

- Finally, there can be direct fiscal/monetary coordination, where the central bank explicitly aims to monetize government programs. This could occur via:

- An increase in debt-financed fiscal spending, where the Treasury isn’t on the hook for the debt because:

- The spending is paired with QE where the central bank retires the debt or commits to rolling the debt forever,

- The central bank promises to print money to cover debt payments (e.g., Germany in the 1930s), or

- Directly giving newly printed money to the government to spend, not bothering to go through issuing debt. Past cases have included printing fiat currency (e.g., Imperial China, the American Revolution, the US Civil War, Germany in the 1930s, the UK during WWI) or debasing hard currency (Ancient Rome, Imperial China, 16th century England).

These MP3 policies support spending in both the private and public sectors. What follows is a laundry list of examples. To be clear, we aren’t recommending any of these; we are just giving you tangible examples.

- QE could be used to purchase real estate or other real goods, which would then ideally be used for socially beneficial ends. For instance, buying up abandoned properties in Detroit (which would support private landholders) and demolishing them to build parks.

- Big debt write-down accompanied by big money creation (the “year of Jubilee”)

- The less direct version of this is via explicitly targeting higher inflation or currency devaluation to lower the real value of the debt over time.

- Central banks explicitly using currency intervention/depreciation as a lever would help with this. For instance, the dollar devaluation during the Great Depression (paired with a law invalidating gold-linked debt) effectively produced a big debt write-off.

- In certain cases, governments directly created or negotiated debt write-downs (e.g., Ancient Rome, Great Depression, Iceland recently).

These MP3 policies are targeted toward the private sector:

- MP3 policies could work through banks, providing them very strong incentives to lend. For instance, in addition to negative rates on excess reserves, the central bank could offer highly positive rates on required reserves—making it materially more profitable for banks to lend (versus building up excess reserves as central banks print money). Flavors of this program have recently been attempted in Europe, Japan, and the UK.

- A different way of accomplishing this is incentivizing households to borrow through subsidized loans or guarantees. One example is the UK’s “Help to Buy” program, providing a five-year, interest-free loan for up to 20% of the property value to some home buyers.

- So far, negative rates haven’t flowed through to households much. Central banks could experiment with explicitly aiming to disincentivize households from holding cash to induce households to spend. For instance, some people have suggested a “carrying tax” on holding cash, at the same rate as the negative interest rate (this was experimented with in Europe during the Great Depression). Other people have suggested invalidating physical money and using digital money only to make it easier to apply a negative interest rate to all cash holdings. Obviously this would be extreme.

- Central banks could be given control over changing income tax rates or sales tax rates, perhaps within a band. They could then use it as an additional countercyclical lever to manage the economy, lowering taxes in recessions (pairing it with money printing) and raising taxes in good times.

- Printing money and doing direct cash transfers to households (i.e., helicopter money). When we refer to helicopter money, we mean directing money into the hands of spenders of money to get them to spend (e.g., US veterans’ bonus during the Great Depression, Imperial China).

- How that money is directed could take different forms—the basic variants are a) to either direct the same amounts to everyone or to aim for some degree of helping one or more groups over others (e.g., to the poorer more than to the rich), and b) to provide this money either as one-offs or over time (perhaps as a universal basic income). These variants could be paired with an incentive to spend it—like the money disappearing if not spent within a year.

- The money could be directed to specific investment accounts (like retirement, education, or accounts earmarked for small business investments) to target it toward socially desirable spending/investment.

- One potential way to craft the policy is to distribute returns/holdings from QE to households instead of to the government.

- As a variant of helicopter money, central banks could give drawdown protection or guarantee a rate of return for stocks and riskier assets in order to further increase asset prices and support spending.

To reiterate, we aren’t offering any comments on the relative merits of these; we are just giving you a sense of the range and the number of historical cases that, if we were in the position of policy makers, we would be looking through. This examination process then has to consider what’s legal, and what’s politically acceptable, in each country. It’s a big job to work out what’s best, so that will take time. As a result, we believe that policy makers, especially central bankers, need to work hard on figuring this out now.

While we won’t offer opinions on each of these, we will offer our opinion that the most effective approach is fiscal/monetary coordination, because it assures that both the providing of money and the spending of it will occur. If central banks just give people money (helicopter money), that’s typically less adequate than giving them that money with incentives to spend the money. However, sometimes it is difficult for those who set monetary policy to coordinate with those who set fiscal policy, in which case other approaches are used.

As we look at these cases, keep in mind that sometimes the policies don’t fall exactly into these categories, as they have elements of more than one of them and they exist on the continuum mentioned above. There is not even a clear line of demarcation between MP2 (i.e., QE) and MP3. For example, if the government gives a tax break, that’s probably not helicopter money, but it depends on how it’s financed. There can be the government acting as the spender, with the central bank financing that spending without a loan—which is helicopter money through fiscal channels.

Part 2: Historical Cases

There are many historical cases of less effective MP1 and MP2 leading to cases of directing monetary policy to put I’d like to show you a bunch of historical cases on MP3 so you get a flavor of how they worked in the past without delving deeply into each because we would have to give you a big book of them to do that. The way I am going to do that is to first dig into Monetary Policy 3 during the Great Depression in the major economies at the time, and then superficially look at several other cases, including some QE cases that are beginning to cross the line to MP3 policies. What I will show you is long but interesting, and it includes how some things that we would consider implausible came about out of necessity. My hope is that in conveying such things we will all be able to open your thinking to a wider range of possibilities than you ordinarily might imagine. Because all of this material is rather long and wonky, I’ve posted it at www.economicprinciples.org for those of you who are interested. But since what happened in the global great depression is the most recent analogous case to today’s environment, I’m including that below if you’d like to examine just one iconic case.

Appendix: Detailed Historical Examples of Monetary Policy 3

We are now going to show you a large number of examples, some explained in more depth than others. They all exemplify the principles about MP3 that we just reviewed. If you find that there are too many, just skip the rest.

Example 1: In the US during the 1930s

As we’ve previously described, President Franklin D. Roosevelt’s policies—especially devaluing the dollar versus gold in 1933—helped create a “beautiful deleveraging.” But by 1935, policy makers were already expressing concern about how the US might offset the next economic downturn. In fact, that year the term “pushing on a string” was coined by a US representative questioning Fed Chair Marriner Eccles, who was concerned that the Fed could stop an expansion but couldn’t do much to offset a contraction. In this section, we describe how the US complemented MP1 and MP2 (low rates and an increase in money) with coordinated, creative fiscal policy—and relied on fiscal and monetary coordination to pull out of the 1937 downturn.

One of Roosevelt’s first major fiscal policy shifts was to engineer big debt write-downs as part of his “beautiful deleveraging” mix. He did that through a couple different policies. First, the US passed a law eliminating the “gold clause” from debt contracts. Up until then, most long-term debts had gold indexation clauses that would have meant the devaluation would increase nominal debt burdens significantly. Eliminating that clause kept debt burdens the same even as the dollar fell, effectively creating a broad-based debt restructuring. Of course, that meant that the government legislated the breaking of contracts in a way that benefited debtors at the expense of creditors. This case was taken to the Supreme Court and decided 5-4 in the government’s favor.

Second, in 1933 Roosevelt created an agency to aid underwater mortgage borrowers, the Home Owners’ Loan Corporation (HOLC). This agency exchanged distressed mortgages for government-guaranteed bonds, purchasing the mortgages above foreclosure value, which encouraged lender participation. Then the HOLC would restructure the mortgages, lowering the interest rate and extending the term of the loan to 15 years (mortgages then typically had a 5- to 10-year maturity). In some cases (though not typically), the HOLC would also reduce the principal to keep the loan-to-value (LTV) ratio for borrowers below 80%. The agency purchased 1 million loans, about 20% of all mortgages, spending $4.75 billion (approximately 8% of GDP).

Roosevelt also created large government programs that directly employed people. The most significant was the Works Progress Administration (WPA), started in 1935. It lasted until the start of World War II and represented spending equal to approximately 2% of GDP annually. The WPA was focused specifically on employment, as it mandated that all projects spend at least 90% of costs on labor. Most projects were infrastructure-related, though there was also funding for white-collar and artistic work. The program hired librarians, musicians, writers, seamstresses, teachers, researchers, doctors, architects, and more. At its peak, it employed about 3.5 million people, over 6% of the labor force.

Further stimulus came in 1936, with a large early payment of a veterans’ bonus. This program is a particularly good example of a government borrowing in order to make direct cash transfers to households. What the governments literally did was to give the veterans non-marketable bonds, which could be exchanged for an immediate payment or held until maturity, paying an above-market discount rate. Also, veterans who had previously borrowed from the government against their future bonus payment received interest forgiveness. Eighty percent of the bonds were cashed in 1936, and the average recipient received approximately $500, more than the median individual annual income at that time. In total, the program represented a fiscal stimulus equal to approximately 2% of nominal GDP. The bonus recipients appeared to have a high tendency to spend the bonus and often used it to make down payments on purchases with credit, like residential investment and car purchases.

Throughout this period, the US rolled out a number of other programs that used fiscal incentives and macroprudential easings to stimulate credit and spending. These programs both supported existing borrowers and encouraged new lending for residential investment:

- In 1932, Congress created the Federal Home Loan Bank System to act as a quasi-central bank and provide funding for S&L banks, and to set underwriting standards and collateral restrictions.

- In 1933, the Home Owners Loan Act provided a federal guarantee to refinance mortgages on homes costing less than $20,000.

- In 1934, the Federal Reserve was given the ability to set margin requirements (Regulation T) to purchase stocks. It began with “extremely lenient” margin requirements (according to a later Federal Reserve report) of 45%, at about the same level as a rule recently introduced by the New York Stock Exchange.

- In 1934, Congress created the Federal Housing Administration (FHA) to insure home loans, which allowed easier underwriting standards (80% LTV and 20-year maturity) for insurance-eligible loans than what the private market was providing. One FHA program insured 20% of loans for improving residential properties, with up to a 5-year maturity.

- In 1934, Roosevelt set up the Electric Home and Farm Authority to provide cheap loans for home electric appliances (under 10% interest rate, 5% down payment) for up to 36 months.

- In 1935, Congress eased LTV and maturity restrictions for national banks (used to be only up to 5-year loans and 50% LTV, now 10-year and 60% LTV).

- In 1937, the Federal Reserve lowered the equity margin requirement to 40% in response to the downturn (it had been increased in 1936).

Roosevelt’s fiscal spending programs were financed by a combination of spending cuts (Roosevelt cut back on the military early in his presidency) and deficit spending. This deficit spending wasn’t primarily financed by direct QE. The persistent gold inflows that followed the US’s devaluation increased the money supply: the banks, unwilling to increase lending to the private sector, significantly increased holdings of government debt to make a nearly guaranteed spread while funding government spending.

Government Response to 1937–38 Downturn

In 1937, the US entered a significant downturn—stocks declined more than 50%, growth turned negative, and the US slipped back into deflation. We won’t discuss the causes of this downturn, as we’ve described them before, but reductions in the WPA employment program and the fading effects of the veterans’ bonus in 1936 were significant contributors, along with devaluations in France and Italy causing dollar appreciation, sterilization of gold inflows, and increasing bank reserve requirements.

In 1938, the US eased monetary and fiscal policy in response to the downturn. In February of that year, Treasury Secretary Henry Morgenthau Jr. ended the gold sterilization program and began desterilizing the accumulated sterilized gold—moves akin to money printing. But policy makers discovered that their actions had very little effect—i.e., they were pushing on a string. From 1938 to 1940, increasing the money supply increased total bank reserves, but the new money was largely held as cash reserves, preventing it from flowing through to the real economy.

The government also passed a $2 billion fiscal stimulus bill, which included a significant increase in the WPA program (it had its biggest year in 1938). While these measures had some effect, the initial improvement in the economy was muted. Industrial production did not recover to peak levels until late 1939, inflation hovered around zero until late 1940, and equities remained approximately 30% below the level of early 1937.

The eventual pickup in economic activity in the US seems largely attributable to World War II. Prior to the US entering the war, production and government spending increased in order to supply the Allies and prepare for potential war. Meanwhile, gold inflows accelerated as investors sought a safe haven from the political situation of Europe and as the Allies began to purchase American supplies (prior to the enactment of Lend-Lease in March 1941).

Eventually, the common cause of World War II united the country and created a political consensus around policies of coordinated and extremely stimulative fiscal and monetary policy. The Federal Reserve summarized its “primary duty” in wartime as “the financing of military requirements and of production for war purposes.” Eccles, who was chair of the Fed through 1948, described his work as “a routine administrative job…The Federal Reserve merely executed Treasury decisions.” During World War II, government spending massively increased, and the money supply more than doubled. The Federal Reserve monetized government spending by maintaining a cap on long-term Treasury bond rates of 2.5% and short-term rates of 0.375%, and by stepping in to buy bonds when rates approached those levels.

Though the world was less globalized in the 1930s than it is now, the debt problems were then (like now) still global and interrelated. We could show you similar developments in a number of countries but, in the interest of brevity, will only touch on what happened in Japan and Germany. Similar things happened in many other countries.

For more historical examples, please visit www.economicprinciples.com

Strategy Consultant | Aspiring Pioneer

3yThanks. Your posts are very informative and elaborate. I wish you wrote in a "top-down" manner, though. But it could just be my preference!

Head of Department in Modern Trade Business Management Program at Faculty of Management Science, Loei Rajabhat University, Thailand

3yThank you for sharing :D

owner Generation Woodworking

3yIt seems the day to day operations of the economy would be best left to a computer program that had current data from all sectors and proscribed the needed actions to deliver the best results for the people. The biggest hurdle would be changing the status quo. Getting the power away from those that have acquired it. The economy has all the money that is needed in it already. No need to inject more, just make what it there move back through the economy. Tax it off the top and put it back at the bottom in the form of higher wages and infrastructure development. Doing that draws the money back to the top. Where it is taxed and brought back to the bottom to be recycled. Don’t let the money collect in one place it must move. Social capitalism.

Investment Engineer and Lawyer

3ySaying #MMT is inevitable is clearly absurd, because MMT was the practice of the US government at the time the statement was made. Treasury and The Fed are part of the same consolidated entity, which in practice has just printed money because the markets have not penalised it with higher rates.

vCFO | Founder: Accountifi | Founder: TheGoodNetwork |

3yRay, thank you for posting your thoughts! Since I am on the margin of understanding the overall theory, I hope that you will be able to address these questions in an upcoming article. What is the overall aim of money in your mind. You talk about sending money to private households or capitalizing development banks. So what is the bigger picture, where does that get us. Are we driving toward higher productivity or more lattes? Does the money need to make us more competitive relative to other economies to be effective? From there, I am concerned that funding government doesnt align interests with efficiency. What motivation does someone have to cut back/find better ways of doing things - if I understand correctly - the goal is to employ people and keep them working. Is now the time to reform the (insert inefficient program/policy here) and reallocate jobs, or just ignore it and keep on as is. The final somewhat unrelated question is around consumer debt. Am I wrong to say that a lot of the money that had been created over the past 30 years has gone to finance lattes, clothing, and vacations? Does part of the fix need to address consumer discretionary spending that winds up in debt (visa/mastercard) or is allocated to industries that have limited impact on productivity? Unproductive student loans? Lack of household savings/investment? Is there a reason to fix these things now, or does this make the problems worse in your mind? Thank you!